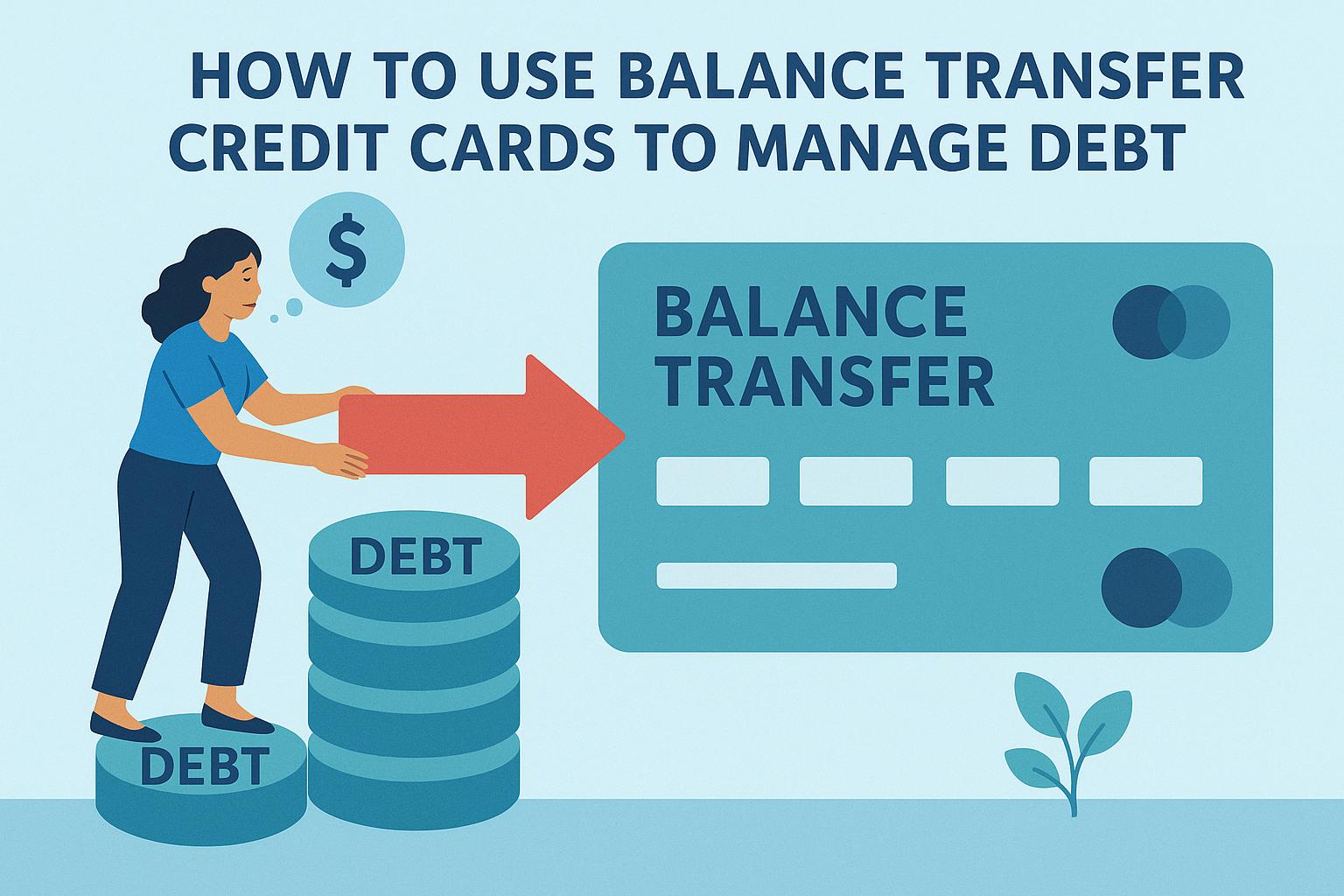

Understanding Balance Transfer Credit Cards

Balance transfer credit cards are a useful financial instrument designed to assist individuals in managing their credit card debt more efficiently. These cards often provide low or even zero-interest rates for a specified introductory period. This allows cardholders to transfer high-interest debt from other credit cards to the new card at a significantly reduced cost. By taking advantage of these lower interest rates, consumers can cut down the amount they pay in interest, thereby facilitating the repayment of the principal balance more easily.

How Do Balance Transfers Work?

Once you are approved for a balance transfer credit card, you gain the ability to transfer existing credit card balances to the new card. Many credit card issuers allow you to move balances from multiple cards, but this is usually limited up to a certain amount. It is vital to understand that most balance transfer offers stipulate that you must complete the transfer within a designated timeframe to benefit from the promotional interest rate.

Balance Transfer Fees

While balance transfer credit cards can be an invaluable resource for managing debt, they often come with associated fees. Generally, a balance transfer fee ranges from 3% to 5% of the amount being transferred. This fee is then added to your new credit card balance. Before proceeding with a transfer, it is crucial to calculate whether the savings you anticipate from the lower interest rate outweigh the cost of the transfer fee.

Comparing Balance Transfer Offers

Not all balance transfer credit cards offer the same benefits or terms. Key factors that should be considered when evaluating different offers include:

– An Introductory Interest Rate: Look for cards that offer 0% APR for the longest duration possible, as it maximizes your potential savings.

– The Duration of the Introductory Period: Introductory periods can range from as short as six months to as long as 21 months. Longer periods provide more time for debt repayment.

– The Standard Interest Rate: Once the introductory period concludes, the interest rate will revert to the card’s standard APR. It’s essential to be aware of what this rate will be to avoid surprises.

– Issuer Limitations: Confirm if the issuer restricts balance transfers from their accounts. Understanding this can help in planning effectively before you apply.

Steps to Use Balance Transfer Cards Effectively

Using balance transfer cards can be immensely beneficial for debt management, but only if they are used properly. Here are some steps to effectively utilize them:

Create a Repayment Plan

Prior to transferring balances, it’s essential to develop a repayment plan. Calculate the monthly payment needed to clear your debt before the end of the introductory period. This strategic approach ensures you capitalize on the savings and avoid the higher interest rate that will apply afterward.

Stick to a Budget

A disciplined budget can prevent further debt accumulation. Balance transfer cards are intended to alleviate existing debt burdens and not serve as a new credit line. Implementing a budget will aid in managing current expenses and preventing future financial difficulties.

Avoid New Purchases

Certain balance transfer credit cards have different interest rates for new purchases made during the introductory period. It is advisable to avoid utilizing the card for new purchases, as it complicates debt repayment by incurring additional interest on new transactions.

Monitoring Your Progress

After you have your repayment plan in place, it’s important to regularly evaluate your progress. Utilizing monthly statements or online account tools allows you to track how much of your principal balance has been paid off. This monitoring process provides motivation and helps ensure you remain on course toward eliminating debt efficiently.

Conclusion

Balance transfer credit cards present a strategic opportunity to manage and decrease credit card debt. By gaining a thorough understanding of how these cards operate, carefully comparing different offers, implementing a deliberate repayment strategy, and maintaining fiscally responsible practices, you can make substantial strides toward financial stability. Nonetheless, it’s critical to stay aware of potential fees and comprehend the terms specific to each card. For more detailed information on managing credit card debt and to explore specific balance transfer card offers, you may want to visit reputable financial advice websites, such as NerdWallet or Bankrate. These platforms provide comprehensive resources and insights that can support your financial journey.