Understanding Your Loan Obligations

A crucial aspect of managing personal finances revolves around comprehending and fulfilling loan obligations. This understanding can significantly impact one’s ability to avoid defaulting on loans. At the heart of managing these responsibilities is familiarizing oneself with the specific terms and conditions associated with the loan. This includes being thoroughly acquainted with the interest rates, repayment schedules, and any penalties associated with late payments. Having this foundational knowledge at your fingertips ensures that you can manage your finances with greater efficiency, thereby avoiding potentially costly surprises down the line.

Interest Rates: These define the cost of borrowing money and can vary significantly between different types of loans and lenders. Being aware of whether your loan has a fixed or variable rate is key, as it affects the predictability of your monthly payments.

Repayment Schedules: These outlines specify when and how much you are required to pay. It is vital to understand these timelines to help plan your financial commitments accordingly.

Penalties for Late Payments: Many loans come with hefty penalties for late payments, which can quickly escalate the total amount owed. Knowing these potential penalties allows you to prioritize timely payments and avoid extra charges.

Developing a Budget

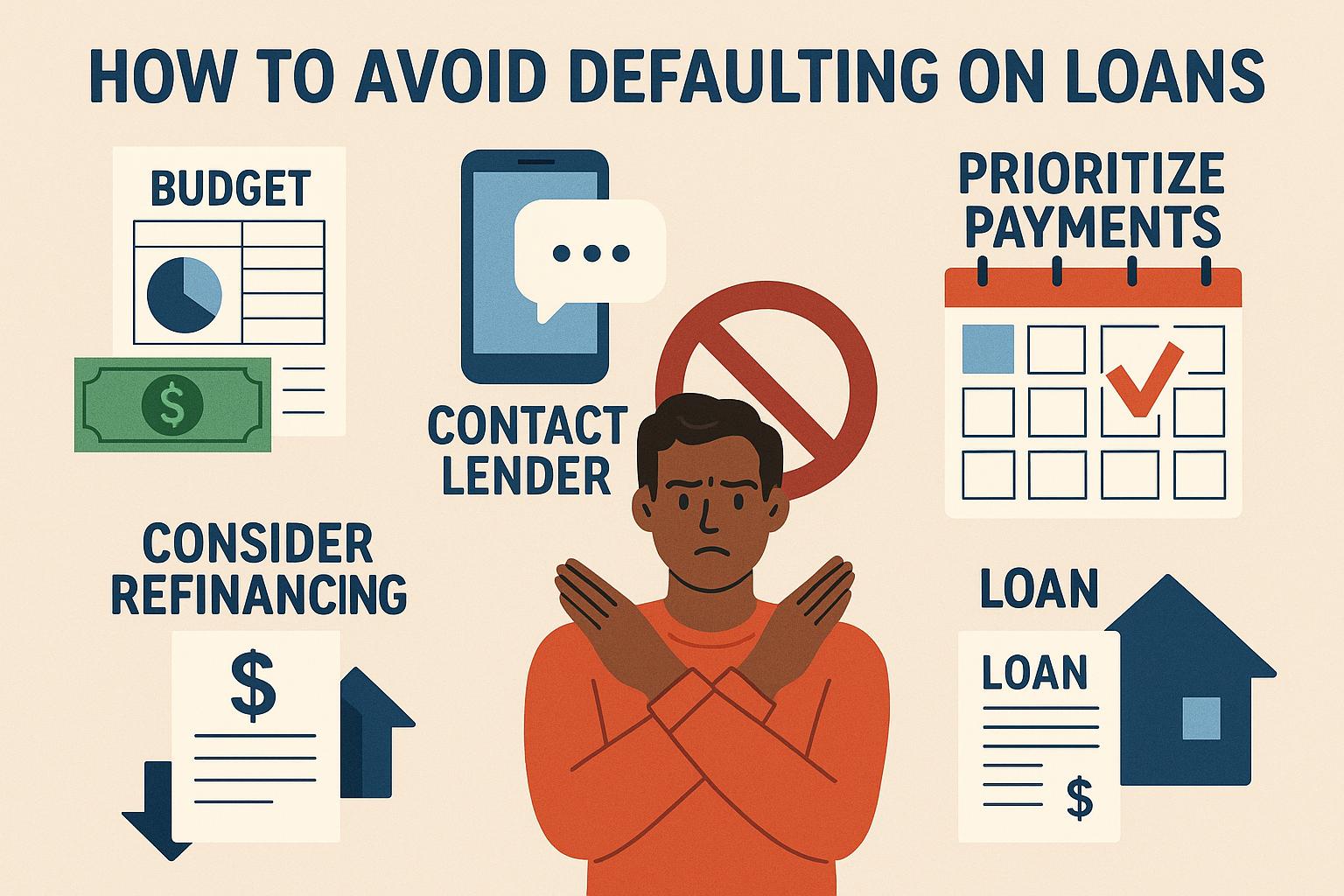

The creation of a viable and realistic budget forms the backbone of effective loan repayment strategies. Budgeting helps ensure that your loan payments are not only made, but made on time. Begin by critically evaluating your income sources and juxtaposing them against your monthly expenses. This process often highlights areas where adjustments might be necessary.

Developing a budget involves prioritizing loan repayments by earmarking specific funds each month explicitly for this purpose. Important: Make it a point to identify and cut out unnecessary expenses from your monthly outflow. Redirect these savings toward fulfilling your loan obligations. The act of budgeting isn’t just about trimming costs but can also enable you to better allocate your resources towards achieving financial stability.

Establishing an Emergency Fund

An emergency fund serves as a vital financial cushion during unpredictable circumstances. Whether you’re faced with sudden medical emergencies or unexpected job losses, having a separate fund can make a significant difference. It can mean the ability to continue making loan payments even when your regular income meets an unexpected disruption. Therefore, it’s advisable to aim for saving at least three to six months’ worth of living expenses within a readily accessible account. This safety net empowers you to maintain stability during volatile financial periods, thereby helping prevent defaults on your loans.

Exploring Refinancing Options

In instances where high-interest rates become challenging, refinancing your existing loan might present a viable alternative. By securing a new loan with more favorable terms, borrowers can effectively decrease their monthly payments, making them more manageable. However, this decision necessitates careful consideration regarding the overall benefits versus the costs involved. Points to ponder: Does refinancing come with prepayment penalties or significant processing fees? Understanding these factors is crucial in determining whether the long-term benefits of refinancing outweigh the potential short-term costs.

Communicating with Your Lender

When faced with anticipated payment difficulties, it’s imperative to engage in early and open communication with your lender. Many lending institutions offer various programs designed specifically to assist borrowers experiencing financial distress. Options may include loan modifications or deferred payment plans tailored to meet specific circumstances. Maintaining an open line of communication with your lender is vital as it can often lead to mutually beneficial solutions which might not have been apparent initially.

Utilizing Financial Counseling Services

In scenarios where managing debts becomes overwhelming, seeking professional assistance from a financial counselor can yield significant benefits. These professionals can provide deeper insights into managing debts and developing personalized strategies aimed at avoiding loan defaults. It’s crucial to enlist the services of accredited counselors who can offer expert guidance on budgeting and efficient debt management to navigate the complexities involved.

Additional Resources

For those eager to delve deeper into loan management and financial stability, additional resources can prove invaluable. Exploring financial literacy organizations or government websites can offer free advice and practical tools to support this endeavor. Online platforms abound with calculators and budgeting apps designed to assist individuals in staying on track with their financial commitments. Furthermore, a visit to your local public library might provide access to financial planning workshops and credible books focused on debt management strategies.

By taking a proactive stance and leveraging available resources, individuals can meaningfully reduce the risk associated with defaulting on their loans. Proactivity, informed decisions, and strategic resource use are central components in this journey toward financial stability and responsibility.